Holding onto a home you need to sell typically costs the average US homeowner between $1,800 and $3,500 every single month once you add up mortgage interest, property taxes, insurance, utilities, and maintenance. In Milwaukee specifically, homeowners insurance now averages between $1,235 and $1,711 per year on a $300,000 dwelling (Policygenius, Bankrate, Insure.com 2026 data), and property taxes consistently rank among the highest in the country. Skip The Agent makes a written cash offer within 24 hours, closes in as few as 7 days, and charges zero fees or commissions, which stops the bleeding immediately for sellers who cannot afford to wait six months for a traditional sale.

If you are sitting on a house you need to sell, whether it is an inherited property in Bay View, a rental in West Allis you are tired of managing, or your own home in Wauwatosa that has become a financial weight, the cost of waiting is not abstract. It is a number you can calculate. And once you see the math written down, the decision to wait or sell becomes much clearer.

This guide is written for one specific reader: the homeowner who owns a home outright or with equity, who needs or wants to sell my house in Milwaukee, and who is trying to figure out whether to list traditionally, wait for a better market, or take a cash offer now. That includes the landlord who just got a $14,000 roof estimate, the executor managing a Milwaukee County probate property from out of state, and the homeowner who is two payments behind and watching the calendar.

We are going to walk through the actual carrying costs line by line, compare a traditional six-month listing against a seven-day cash close with real numbers, and tell you honestly when each path makes sense. If a traditional listing is the right move for your situation, we will say so.

The Five Costs Every Homeowner Underestimates

Most sellers calculate the cost of owning a home as “my mortgage payment.” That number is a fraction of the real total. Here are the five categories that make up your true monthly carrying cost.

1. Mortgage Interest (Not Principal)

If you still owe a mortgage, only a portion of each payment builds equity. The rest is pure expense. On a $250,000 mortgage at 6.1% (the current Milwaukee-area average per February 2026 market data), your monthly payment is roughly $1,515 for principal and interest. Of that, about $1,270 in the first year is interest, money you will never see again.

If you are early in your loan, interest can account for 80 to 85 percent of your monthly payment. For a home you are trying to sell, this is dead money.

2. Property Taxes

Wisconsin consistently ranks in the top ten states for effective property tax rates. Milwaukee County’s effective rate runs around 2.3 to 2.5 percent of assessed value, meaningfully higher than the national average of roughly 1.1 percent.

On a $300,000 Milwaukee home, that is approximately $7,000 to $7,500 per year, or $580 to $625 per month. Every month you hold the property, that meter keeps running, whether or not anyone is living there.

3. Homeowners Insurance (And It Is Climbing)

Here is where Milwaukee homeowners are getting hit especially hard in 2026:

- Policygenius / Hippo (2026): $1,235/year for a $300,000 dwelling

- Bankrate (2026): $1,381/year for the same coverage in Milwaukee

- Insure.com (2026): $1,711/year with $100k liability and a $1,000 deductible

The realistic range for a Milwaukee homeowner with a typical $300,000 dwelling policy in 2026 is $1,235 to $1,711 per year, or roughly $103 to $143 per month. For older homes, homes with older roofs, or homes with prior claims, that number can climb significantly higher.

Homeowners insurance in Milwaukee averages between $1,235 and $1,711 per year for a $300,000 dwelling in 2026, according to Policygenius, Bankrate, and Insure.com data. Vacant home insurance, required when a property sits empty for more than 30 to 60 days, typically costs 50 to 75 percent more than a standard policy. That means an inherited or unoccupied Milwaukee home can easily run $2,000 to $3,000 per year in insurance alone.

If the home is vacant, your standard policy almost certainly will not cover it. We have seen this catch executors and out-of-state heirs by surprise more than any other carrying cost. For more on this, our analysis of Home Insurance Rates Are Rising Fast in the Midwest: What That Means If You Own an Older Home breaks down what insurers are doing in 2026.

4. Maintenance and Deferred Repairs

National data suggests homeowners should budget 1 to 4 percent of home value per year for maintenance. On a $300,000 home, that is $3,000 to $12,000 annually, or $250 to $1,000 per month.

For Milwaukee specifically, the housing stock skews older. A large share of homes were built before 1960, which means original mechanicals, plaster walls, knob-and-tube remnants, lead paint disclosures, and roofs that are at or past their service life. If you are sitting on deferred maintenance, the cost is not zero. It is a clock that is ticking toward a much larger bill.

5. Opportunity Cost (The Hidden One)

If your home has $150,000 in equity sitting in it, that money is earning nothing. If you sold and parked it in a high-yield savings account at 4 percent, you would earn $500 per month in interest. If you invested it conservatively at 6 percent average returns, you would earn $750 per month.

That is real income you are not collecting. It does not show up on any bill, but it is a cost.

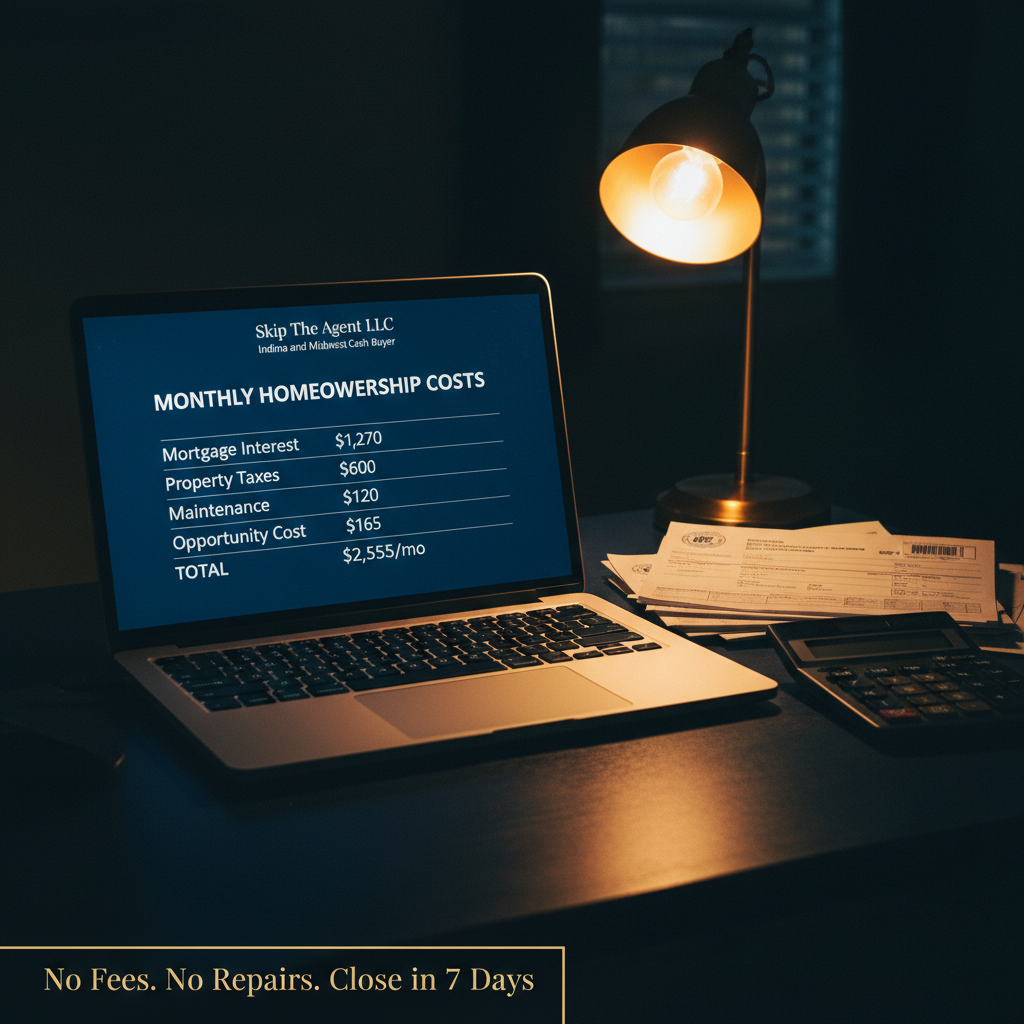

The Total: What Holding Really Costs You Per Month

Let us add it up for a typical $300,000 Milwaukee home with a $250,000 mortgage:

- Mortgage interest: $1,270

- Property taxes: $600

- Insurance: $120 (or $200+ if vacant)

- Maintenance reserve: $400

- Opportunity cost on $50,000 equity: $165

Total: roughly $2,555 per month, or about $30,660 per year.

For a paid-off home with $300,000 in equity:

- Property taxes: $600

- Insurance: $120

- Maintenance: $400

- Opportunity cost on $300,000 equity: $1,000

Total: roughly $2,120 per month, or about $25,440 per year.

These are not worst-case numbers. They are average numbers for an average Milwaukee home. Now let us look at what a traditional sale actually costs and how long it actually takes.

Traditional Listing vs. Cash Sale: The Six-Month Math

Wisconsin REALTORS® Association data from January 2026 shows tightened inventory and rising prices in the Milwaukee real estate market, with the metro median sold price around $379,900. That sounds like good news for sellers, and for some sellers it is. But “median days on market” and “time from decision to cash in hand” are very different numbers.

Here is what a traditional sale realistically looks like from the day you decide to sell to the day funds hit your bank account:

Traditional Listing Timeline (National Averages)

- Weeks 1 to 4: Prep, clean, repair, stage, photograph, list

- Weeks 5 to 12: Active listing, showings, offers

- Weeks 13 to 16: Accepted offer, inspections, appraisal, financing contingencies

- Weeks 17 to 20: Closing

That is 4 to 5 months on the fast end. National median time from listing to closing has hovered around 70 to 90 days, and that does not include the prep period before the home goes live.

Traditional Listing Cost Breakdown on a $300,000 Sale

- Agent commissions (5 to 6 percent): $15,000 to $18,000

- Pre-listing repairs and updates: $5,000 to $15,000

- Staging and professional photos: $1,500 to $3,000

- Seller concessions (now common again): $3,000 to $9,000

- Closing costs (title, transfer, prorations): $2,000 to $4,000

- Six months of carrying costs while listed: ~$15,000

Total cost of a traditional sale: $41,500 to $64,000

Your net on a $300,000 sale, traditionally listed, lands somewhere between $236,000 and $258,500.

For a deeper breakdown of every fee involved, our article on What Does It Actually Cost to Sell a House? Every Fee Explained shows the full picture.

Skip The Agent: The Cash Sale Math

A cash offer on the same home will not match the retail listing price. We do not pretend otherwise. A fair cash offer typically lands at 80 to 88 percent of after-repair market value, depending on the condition of the home and the work it needs.

For a $300,000 Milwaukee home in average condition needing roughly $20,000 in updates, cash home buyers in Milwaukee like Skip The Agent calculate offers this way:

- Cash offer: $240,000 to $255,000

- Agent commissions: $0

- Repairs: $0 (we buy as-is)

- Staging, cleaning, photos: $0

- Closing costs paid by seller: $0

- Carrying costs (7-day close): ~$600

Net to seller: $239,400 to $254,400 in roughly 7 to 14 days.

Side-by-Side Comparison

| Traditional Listing | Skip The Agent | |

|---|---|---|

| Gross sale price | $300,000 | $240,000 to $255,000 |

| Commissions | $15,000 to $18,000 | $0 |

| Repairs and prep | $6,500 to $18,000 | $0 |

| Closing costs (seller side) | $2,000 to $4,000 | $0 |

| Carrying costs during sale | ~$15,000 | ~$600 |

| Time to cash | 4 to 6 months | 7 to 14 days |

| Estimated net | $236,000 to $258,500 | $239,400 to $254,400 |

The gap is much smaller than most sellers expect. And once you factor in uncertainty, deal fall-through risk, and the emotional cost of six months of showings, the math gets even closer.

To run the numbers on your specific property, you can get a free estimate here.

When a Cash Sale Is NOT the Right Choice

We are going to be direct about this because it matters. A cash sale is not the best move for everyone, and pretending otherwise is how the industry earned its reputation.

List with an agent if:

- Your home is in strong, move-in-ready condition in a desirable neighborhood. You will likely net more on the open market, even after commissions.

- You have 6+ months of runway financially and emotionally. No foreclosure timeline, no probate deadline, no divorce decree forcing a sale.

- You do not have significant deferred maintenance that will scare off financed buyers or kill the appraisal.

- You can live elsewhere during showings or you are comfortable with strangers walking through your home for months.

- The home is not a rental with a difficult tenant in place. Vacant or owner-occupied homes show better and sell faster.

If three or more of those describe your situation, list traditionally. You will likely come out ahead.

A cash sale makes sense if:

- You are facing a hard deadline: foreclosure, sheriff sale, probate court, divorce settlement, or job relocation.

- The home has significant repairs that you cannot or do not want to fund.

- The property is vacant and bleeding carrying costs every month.

- You are a landlord ready to be done, especially with tenants in place.

- You value certainty and speed over squeezing out the last 5 to 10 percent of value.

If you are in the second group, the math we just walked through is exactly why working with companies that say “we buy houses in Milwaukee” exists as an option. It is not a discount product. It is a different product.

The Hidden Cost of Distress: Foreclosure and Probate Timelines

If you are behind on payments or managing an estate, the carrying cost math changes dramatically because the clock is no longer yours.

In Wisconsin, foreclosure is a judicial process that typically takes 9 to 14 months from first missed payment to sheriff sale. Milwaukee foreclosure homes that reach the sheriff sale stage have usually cost the owner tens of thousands in accumulated fees, penalties, and credit damage before any equity is recovered. By the time the sheriff sale happens, the homeowner has usually lost any chance of recovering equity.

Probate in Wisconsin typically takes 6 to 12 months for an uncontested estate, during which the property must continue to be insured (often with a vacant home policy), taxes must be paid, and maintenance handled. Out-of-state heirs often spend $10,000 to $20,000 just maintaining a property they never wanted, only to net less than expected after probate fees.

If you are in either of these situations, the carrying cost is not your only enemy. The timeline is. Our guides on How to Stop Foreclosure on Your Home: Every Option Explained and Selling an Inherited House: A Complete Guide for Heirs go deeper on each. For direct human help, you can contact our team here.

What “Affordable” Actually Means When You Already Own

Most homeowners ask “what house can I afford” when they are buying. Fewer ask the more important question once they already own: can I afford to keep this one?

If carrying costs are consuming more than 30 percent of your household income, if you are dipping into savings to cover the mortgage, or if a single major repair would put you underwater, the answer may be no. And that is not a failure. That is a financial reality that deserves a clear-eyed decision.

The worst outcome we see is homeowners who wait too long. They burn through savings, miss payments, damage their credit, and then sell in distress for less than they would have gotten six months earlier. The cost of waiting is almost always higher than the cost of acting.

The Bottom Line

Holding a home you need to sell costs the average Milwaukee homeowner roughly $2,000 to $2,500 per month once you count every line item, more if the home is vacant or needs work. Over a six-month traditional listing, that is $12,000 to $15,000 just to keep the lights on while you wait.

If you have time, equity, and a move-in-ready home, list it. Take the higher gross. Pay the commissions. Net more in the end.

If you want to sell your house fast in Milwaukee and are facing a deadline, a repair list, a tired rental, or a property you simply need to be done with, a cash offer stops the bleeding immediately. Skip The Agent makes a written offer within 24 hours, closes in as few as 7 days, and charges zero fees, zero commissions, and zero closing costs to the seller. We buy as-is. No repairs, no cleaning, no staging.

If you want to know what your home is worth as a cash sale, request a free estimate or contact our team directly. We will give you the math, walk you through the offer logic, and tell you honestly whether a cash sale or a traditional listing is the better path for your situation.

Frequently Asked Questions

How much does it cost per month to hold a vacant house?

A vacant home typically costs the owner $1,800 to $3,500 per month nationally once you add mortgage interest, property taxes, insurance, utilities, and maintenance. In Milwaukee specifically, taxes run higher than the national average, and vacant home insurance can cost 50 to 75 percent more than a standard policy, pushing the monthly carrying cost on a vacant $300,000 home toward the high end of that range.

Why is homeowners insurance going up so much in 2026?

Insurers are raising rates because of higher claims costs from severe weather, climbing repair and labor expenses, and reinsurance market pressure. In Milwaukee, 2026 rates for a $300,000 dwelling range from $1,235 to $1,711 per year depending on the carrier, with older homes and homes with prior claims paying significantly more.

What percentage of market value do cash buyers typically offer?

Reputable cash buyers typically offer 80 to 88 percent of after-repair market value, with the exact number depending on the home’s condition, location, and the cost of repairs needed. Offers below that range are usually lowball offers from buyers who expect to be negotiated up, and offers above that range often come with hidden fees, financing contingencies, or last-minute price reductions before closing.

Is it better to list with an agent or sell to a cash buyer?

List with an agent if your home is in strong condition, you have at least six months of financial runway, and there is no deadline forcing a sale. Sell to a cash buyer if you are facing foreclosure, probate, divorce, or relocation deadlines, if the home needs significant repairs, or if you simply value speed and certainty over squeezing out the last 5 to 10 percent of value.

How long does a traditional home sale actually take from start to finish?

A traditional home sale takes 4 to 6 months from the decision to sell to funds in your bank account, including 2 to 4 weeks of prep and repairs, 6 to 8 weeks on the market, and another 4 to 6 weeks from accepted offer through closing. National median days on market plus closing time has run between 70 and 90 days throughout 2025 and into 2026, and that does not include pre-listing preparation.

Can I sell a house that has code violations or major repair issues?

Yes, you can sell a house with code violations or major repairs by selling to a cash buyer who purchases as-is, since most retail buyers using financing cannot close on homes with significant issues. Lenders typically require homes to meet minimum property standards for FHA, VA, and conventional loans, which means homes with structural, electrical, plumbing, or roof problems often have to sell to cash buyers or investors.

What happens to my property taxes and insurance if the house sits empty?

Property taxes continue to accrue exactly the same whether the house is occupied or vacant, and most standard homeowners insurance policies automatically void coverage after 30 to 60 days of vacancy. To stay covered on a vacant home you need a vacant home policy, which costs 50 to 75 percent more than a standard policy and provides more limited coverage.

How quickly can a cash sale actually close?

A legitimate cash sale can close in 7 to 14 days from offer acceptance, since there is no lender, no appraisal contingency, and no financing timeline. Skip The Agent makes a written offer within 24 hours of inquiry, can close in as few as 7 days, and lets the seller choose the closing date if more time is needed for moving or other arrangements.

Written by Addai Lewellen and Grant Umali, co-founders of Skip The Agent LLC. Addai brings deep experience in real estate acquisitions and deal structuring across Midwest and national markets. Grant brings a background in marketing, sales, and customer success. They handle every deal personally. Reach them directly at skiptheagent.llc.

Want to skip the carrying costs? We close in as few as 7 days.

Get a free, no-obligation offer in 24 hours — from two real people, not an algorithm.

Get My Free Cash OfferCloses in as few as 7 days · No repairs needed · 100% free to request

Not ready to call yet?

Get our latest market updates, seller guides, and real estate insights delivered straight to your inbox. No spam, no pressure.

One email. No spam. No pressure.